An equity line of credit on commercial property is a financial tool that allows property owners to access funds based on the equity in their commercial real estate. This revolving credit line provides flexibility for business owners to draw funds as needed, using the property’s value as collateral. Interest is typically variable, and repayment terms are structured based on the borrowed amount.

Read on because this article unveils the untapped potential of equity lines of credit for commercial properties, equipping you with the knowledge needed to capitalize on lucrative opportunities.

Whether you need working capital, want to reinvest in your property, or seeking an alternative to high-interest debt, a commercial equity line can be a game changer. Let’s delve in and uncover how to tap into your equity to take your business to new heights!

Key Takeaways

- Equity lines allow real estate investors to access capital for property improvements, maintenance, renovations, or operating expenses.

- Commercial equity lines differ from unsecured mortgage loans by using real estate as collateral instead of business assets or owner guarantees.

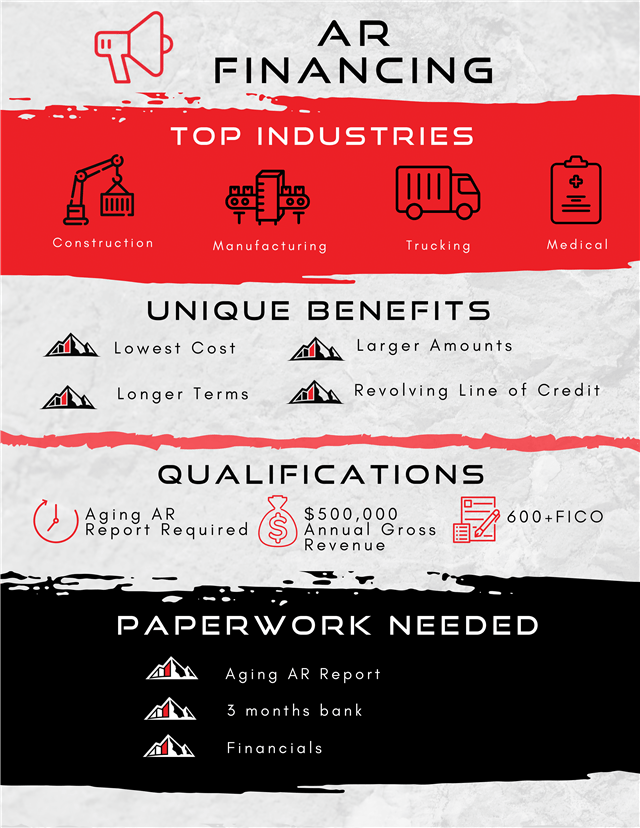

- Multi-tenant buildings with reliable income streams are ideal property types for equity line borrowing.

- Specialized lenders like credit unions and private lenders often offer lower rates than big banks for commercial equity lines.

Eligibility Criteria: What You’ll Need to Leverage and Qualify for Capital

Obtaining a CELOC involves an application and approval process similar to other commercial loans. Lenders will evaluate key factors to determine your eligibility, such as:

Credit History – A strong personal credit score (680 and above) demonstrates financial responsibility and boosts chances for approval. Resolve any errors on your credit report and pay down existing debts to improve your score.

Property Value – The lender will require a professional appraisal to establish property value and the amount of equity available to borrow against. Target a property with significant existing equity.

Loan-to-Value (LTV) Ratio – The percentage comparing loan amount to appraised property value. A lower LTV signals lower risk for lenders (usually 80% LTV or less).

Debt-to-Income (DTI) Ratio – Your total monthly debt payments divided by gross monthly income. A DTI below 50% improves approval odds.

Financial Documentation – Lenders will review business and personal tax returns, profit and loss statements, balance sheets, business licenses, and bank statements to verify assets, income, and ability to repay.

Business Standing – Having an established successful business, strong revenue history, and solid business credit score can offset other deficiencies in your application.

Property Type – Commercial real estate like retail, office buildings, industrial warehouses, and multifamily apartment complexes tend to qualify more easily than specialized properties.

Location – Properties located in economically thriving areas are preferred over distressed locations.

With a clear picture of eligibility criteria, you can determine if a CELOC aligns with your financial situation. Consulting a qualified business loan broker can also help navigate the process.

Table 1: Comparing Commercial Equity Lines to Other Financing Options

| Financing Type | Interest Rates | Collateral Required | Term Length | Use of Funds |

|---|---|---|---|---|

| Commercial Equity Line | Variable, Prime + margin | Commercial property | Revolving credit line, up to 10 years | Flexible business purposes |

| SBA Loan | Below market fixed rates | Business assets | 5-25 years | Real estate, equipment, working capital |

| Commercial Mortgage | Fixed rate | Commercial property | 5-30 years | Real estate purchase or refinance |

| Merchant Cash Advance | Very high, factor rate | Credit card receivables | 6-12 months | Working capital |

Strategic Uses: How to Tap Your CELOC to Grow Your Business Using our Financial Services

The flexibility and revolving access of a CELOC offers advantages for several growth-oriented business needs:

Business Owners Funding Operating Expenses and Smoothing Cash Flow

- Access capital quickly without depleting cash reserves

- Bridge income gaps and seasonal dips in revenue

- Avoid high interest costs of cash advances or merchant loans

Expanding Operations and Opening New Locations

- Open an additional location or office space

- Hire more staff to meet growing demand

- Purchase specialized equipment or fleet vehicles

Renovating Commercial Property

- Finance maintenance, repairs, and upgrades

- Remodel to create more appealing space for customers/tenants

- Add amenities like parking, landscaping, or signage

Equity Line of Credit on Commercial Property: Refinancing Costly Debt

- Pay off credit cards, equipment loans, or merchant cash advances

- Consolidate higher interest short-term debts into one lower monthly payment

Purchasing Business Assets

- Acquire a competitor’s book of business

- Buyout a partner or co-owner’s ownership stake

- Purchase specialized equipment to boost capabilities

Seizing New Market Opportunities

- Bid on profitable contracts or accounts

- Acquire a complementary business to expand offerings

- Invest in new technology, intellectual property, or inventory

Each draw against your CELOC can fuel key strategic moves to help your business capture market share, boost profits, and outpace competitors.

Optimizing Taxes and Audits with Commercial Equity Loans

Beyond fueling growth, the interest paid on a CELOC may provide tax reduction opportunities:

- Interest Expense Deductions – Interest paid is generally tax deductible as a business expense. Consult a tax professional to maximize deductions.

- 1031 Exchange – You can use CELOC funds to purchase another “like-kind” commercial property and defer capital gains taxes on the sale of your current property.

- Primary Residence Conversion – Convert to a primary residence for two years before selling to qualify for the capital gains home sale exclusion. Use the CELOC to make property improvements.

- Investing Gains – Rather than paying capital gains taxes on a commercial property sale, use the proceeds to invest in an opportunity zone fund or renewable energy projects.

Work closely with your tax accountant and lender to implement the optimal tax minimization strategy for your situation. The interest savings could justify the cost of a CELOC.

Generating Passive Income with a Commercial Equity Loan

A CELOC opens the door to potentially lucrative passive income streams:

- Buy and Lease – Use funds to acquire an additional commercial property and lease it to a tenant to generate monthly rental income.

- Rent out Space – Convert unused space in your existing property into leasable units, storage, billboards, cell towers, etc.

- Invest Idle Cash – Rather than let equity sit idle, invest CELOC funds into dividend stocks, peer-to-peer lending, REITS, or other income-generating assets.

- Launch Side Business – Seed funding for a new online business, information products, vending machines, or other semi-passive ventures.

- Invest in Existing Business – Automate processes and outsource roles in your current business to increase free cash flow.

Consult with financial and legal advisors to create the optimal passive income strategy tailored to your market, assets, and capabilities. The key is leveraging capital to work harder for you.

| Objection | Response |

|---|---|

| I’m concerned about providing personal financial information like my Social Security number. | I understand your concern. We only request essential information to process your application, and we take data security very seriously. We use encryption and secure servers to protect your personal data. |

| What if I want to pay off my equity line of credit early? | Our equity lines of credit have no prepayment of loan penalties, so you’re welcome to pay it off early with no additional fees. |

| This sounds risky – could I lose my commercial property if I default? | Our equity lines use your property as collateral, but we don’t take ownership if you default. We’d work with you on repayment options before resorting to foreclosure. |

| How soon can I access funds if I apply for an equity line of credit? | Our streamlined approval process allows us to provide funding in as little as 1-2 weeks. We know quick access to capital is key. |

| What are the tax implications of using an equity line of credit? | The interest is usually tax deductible as a business expense. We recommend consulting a tax advisor regarding your specific situation. |

Getting a CELOC as a Safety Net for Business Continuity

The unexpected can put any business at risk – economic downturns, supply chain disruptions, loss of a major customer, or natural disasters. A CELOC can provide a financial lifeline to weather turbulent times by:

- Providing quick access to capital to cover operating costs if revenues slow.

- Funding disruption response like temporary relocation, equipment repairs, or bringing on contract workers.

- Smoothing out financial impacts while recovering and returning to normal operations.

- Avoiding desperate expensive measures like high-interest loans or liquidating assets at a loss in a down market.

No entrepreneur wants to consider worst case scenarios, but hoping for the best without planning for the worst can sink a business. Knowing you have reserve capital waiting in the wings provides tremendous peace of mind.

Case Studies

The COVID-19 pandemic has reverberated across various sectors, significantly impacting commercial real estate prices.

A comprehensive study titled “A first look at the impact of COVID-19 on commercial real estate prices: Asset-level evidence” provides valuable insights into the aftermath of the pandemic on the real estate market.

This research delves into asset-level evidence, shedding light on the nuanced consequences of the global crisis.

Volatility in Real Estate Equity Returns During COVID-19

Cross-Sectional Analysis

Another pivotal aspect of the pandemic’s influence on the real estate sector is explored in the study “Volatility and the cross-section of real estate equity returns during Covid-19”.

This research conducts a cross-sectional analysis, offering a detailed examination of the volatility in real estate equity returns.

Understanding the dynamics of these fluctuations is crucial for comprehending the challenges and opportunities within the commercial real estate landscape.

Macroeconomic Factors and Stock Prices in Vietnam Real Estate

A Case in Vietnam

Examining the impacts of internal and external macroeconomic factors on firm stock prices within the Vietnam real estate industry, the research explores an expansion econometric model.

This case study provides a valuable perspective on the interplay between broader economic forces and the specific dynamics of the real estate market in Vietnam.

Banking Credit Restructuring Policies in Indonesia Amid COVID-19

Financial Strategies

As financial institutions navigate the challenges posed by the pandemic, the study on banking credit restructuring policies in Indonesia offers insights into adaptive strategies amid the COVID-19 pandemic.

Understanding how banks reshape their credit policies can be instrumental in anticipating shifts in commercial property financing.

Reshaping Retail Real Estate and High Streets Post-COVID-19

E-commerce and Digitalization

In the context of commercial property, the research on how the COVID-19 pandemic would reshape retail real estate and high streets through the acceleration of E-commerce and digitalization is particularly relevant.

This study explores the transformative impact of digital trends on the retail sector and, by extension, on commercial properties.

Finding the Best CELOC Terms from the Right Lender

All CELOCs are not created equal. As you evaluate offers, look for features like:

- Low Interest Rates – The lower the rate, the more you save in interest fees. Variable rates around Prime + 1% are ideal.

- High Credit Limit – Securing a higher limit provides more growth capital over time.

- Long Draw Period – Multi-year draw periods (10 years+) give flexibility to access funds as needed.

- Interest-Only Payments – Paying interest-only while drawing funds preserves capital.

- Low Fees – Origination/application fees below 3% of the credit limit are reasonable.

- No Prepayment Penalties – Avoid lenders charging fees for early payoff.

Commercial lenders come in many shapes and sizes, from big banks to specialized CELOC lenders.

Work with a reputable broker to shop around and negotiate the best possible deal.

The right financing partner can make a big difference in the success of your CELOC.

Multifamily Cash with a Real Estate Loan Specialist

As a real estate investor interested in multifamily residential properties, working with a loan specialist can help you access the capital needed to purchase or improve your assets. There are several financing options to consider:

- Fannie Mae provides loan programs for the acquisition, refinancing, or renovation of multifamily properties. These amortizing loans offer competitive interest rates and flexible terms.

- Bridge loans can provide quick capital for multifamily purchases before securing permanent debtor financing. The loans are typically 6-24 months with interest-only payments.

- Commercial home equity lines of credit (HELOCs) allow you to access revolving funds by tapping your property’s equity. The credit line is secured by the asset’s value.

- Private equity firms may fund value-add multifamily projects in exchange for an ownership stake and preferred return. This brings expertise and capital for renovations.

A knowledgeable loan specialist can help analyze your business opportunity and net worth to match you with the optimal cross-collateralization and financing mix. Their industry connections can facilitate loan origination and escrow services as well.

Mezzanine Debt for Industrial Properties

Mezzanine loans are a flexible form of subordinate debt that can help fund industrial real estate projects. Here are some key benefits for industrial property investors:

- Provides additional capital beyond senior loans for acquisitions, expansions, or renovations.

- Typically does not require personal guarantees like other junior debt options.

- Allows the sponsor to retain greater ownership and control compared to joint venture equity.

- More flexible qualifications than senior lenders and quicker to execute than raising equity.

- Interest payments are typically cash-flow based instead of requiring principal reductions.

- May include warrants or equity participation to boost investor returns if property performs well.

With strong demand for industrial facilities, mezzanine lenders see this sector as attractive for flexible subordinate debt investments. The loans fill a funding gap between senior debt and equity to leverage returns.

Avoiding Pitfalls: How to Manage your CELOC Responsibly

While CELOCs provide small businesses with game-changing capital access, they do come with inherent risks to manage:

- Don’t Tap Out Your Equity – Limit draws to 75-80% loan-to-value so you don’t get overextended.

- Have a Repayment Plan – Know where cash will come from to make monthly interest payments and pay down principal.

- Monitor Property Value – If the market declines, you may have less equity borrowing capacity over time.

- Watch for Cross-Default Triggers – Defaulting on another loan related to the property can trigger CELOC default.

- Maintain Strong Business Performance – Poor financials increase default risk if cash flow stumbles.

By monitoring equity levels, cash flow, credit scores, and property value, you can take preventive steps if warning signs appear. The key is striking the right balance between leveraging equity and managing risk.

Table 2: Commercial Property Types Often Used for Equity Lines

| Property Type | Typical Loan-to-Value Ratio | Drawbacks |

| Retail Storefront | 70-80% | Tenant turnover risk |

| Warehouse | 75-80% | Localized market dependence |

| Office Building | 75-80% | Longer lease terms required |

| Apartment Building | 75-85% | Higher management costs |

| Hotel | 65-75% | Tourism market reliance |

Additional Benefits and Use Cases for Real Estate Investors

For real estate investors, equity lines of credit offer a wide range of potential benefits beyond those already outlined. These lines of credit can provide flexible short-term financing for minor repairs or renovations to commercial properties in an investor’s portfolio.

The funds can be used to refresh tenant spaces when turnover occurs, enhancing leasing potential. Lines of credit offer fast access to capital for unexpected expenditures like a roof replacement or HVAC failure.

For major redevelopment projects, an equity line can serve as a bridge loan until longer-term financing is secured. The flexibility of CELOC is well suited to the fluid capital needs inherent in commercial real estate ownership and investing.

Comparison to Other Common Real Estate Financing Options

Equity lines of credit represent just one type of financing that real estate owners can utilize.

They differ significantly from other options like traditional commercial mortgages and have pros and cons versus alternatives like unsecured business lines and hard money loans.

For example, CELOCs can provide faster access to capital compared to commercial mortgages, which often take 30-60 days to close. However, rates on equity lines are typically higher than those for conventional mortgages or SBA 504 loans.

Weighing the tradeoffs based on your specific business objectives is key to identifying the optimal financing solution.

Ideal Candidates for Commercial Equity Lines

While equity lines can benefit a wide range of business owners, they tend to be most advantageous for those who:

- Have significant existing equity in commercial property assets

- Need flexible revolving financing for unknown future needs

- Seek to avoid dilution, loss of control, or collateral risks of equity investors or unsecured loans

- Require speed and flexibility not offered by traditional mortgages and SBA loans

- Can repay draws within 5-10 years before end of draw period

Businesses meeting these criteria are best positioned to strategically utilize equity line financing to seize timely business opportunities as they arise.

Commercial Equity vs. Home Equity Lines

Real estate owners sometimes consider tapping home equity lines instead of commercial equity, but important differences exist.

While home equity lines generally have lower rates and fees, they limit the use of funds to the home itself. In contrast, commercial equity lines have higher limits and the funds can be deployed freely into business purposes.

The business purpose requirements also allow commercial equity line interest to be tax deductible, unlike home equity lines.

And defaulting on a home equity loan could place the owner’s residence at risk, while commercial equity lines avoid that exposure.

Ideal Properties for Commercial Equity Lines

While most commercial real estate types are eligible, some property segments are better suited for equity line borrowing:

- Multi-tenant buildings with reliable rental income

- Professional office spaces with longer-term tenants

- Industrial facilities in active warehouse markets

- Self-storage facilities with high occupancy rates

- Hospitality properties in high-traffic tourism markets

Such properties provide asset stability and reliable cashflow to support equity line borrowing. Meanwhile, more volatile or distressed assets would carry higher risk.

Commercial Equity Line Interest Rates

Interest on commercial equity lines typically follows a variable rate tied to the Prime Rate or LIBOR benchmark.

Rates consist of the index rate plus a margin determined by the lender’s risk assessment.

Strong borrowers may qualify for Prime + 0.5% up to Prime + 2%. By comparison, alternatives like unsecured business lines or merchant cash advances can carry rates from 7-15%.

The lower cost of capital makes commercial equity lines attractive for well-qualified borrowers with substantial equity.

Lending Sources for Commercial Equity Loans

While large banks do offer them, small businesses may find better commercial equity line options through:

- Specialized commercial mortgage brokers

- Credit unions offering commercial lending

- Non-bank and alternative commercial lenders

- Private lending groups and investors

Working with knowledgeable real estate loan specialists can help navigate the range of lenders and identify ones most amenable to your particular situation.

Table 3: Average CELOC Rates From Different Lender Types

| Lender | Rate (Prime + Margin) |

|---|---|

| Big Banks | Prime + 1-2% |

| Credit Unions | Prime + 0.5-1.5% |

| Alternative/Non-bank Lenders | Prime + 1-3% |

| Private Lenders | Prime + 2-4% |

I once helped a manufacturing company that needed additional capital to expand their operations and take advantage of the booming real estate market.

They owned several industrial properties that had appreciated in value over the years, but they did not want to sell them or take out a traditional loan that would require monthly payments and a fixed interest rate.

They wanted a flexible and convenient way to access cash as needed, without affecting their cash flow or profitability.

That’s when I suggested them to apply for a commercial equity line of credit (CELOC), a type of loan that uses owner-occupied commercial real estate as collateral and provides a revolving line of credit that can be drawn and repaid as desired.

I explained to them the benefits and risks of CELOC, such as the lower interest rate, the longer repayment period, the tax deduction, and the possibility of foreclosure. I also helped them prepare the required documents, such as their credit score, their loan-to-value ratio, their nonrecourse debt-to-income ratio, their balance sheet, their financial statement, and their property appraisal.

I then connected them with several reputable lenders that offered competitive rates and terms for CELOC. After comparing the offers, they chose the one that suited their needs and goals the best. They were approved for a CELOC of $2 million, which they used to purchase new heavy equipment, renovate their facilities, and invest in new opportunities.

They were very happy with the outcome and thanked me for my assistance.

Exit Strategy for Commercial Equity Lines

One key consideration in utilizing a commercial equity line is having an exit strategy to repay the outstanding balance before the draw period expires. Some options include:

- Paying down gradually over time from business cash flows

- Refinancing into longer-term mortgages or SBA business equity loans

- Liquidating the property or 1031 exchange into another

- Bringing in an equity partner for a buyout

Carefully projecting capital needs and timing for each draw can help ensure payback aligns with your exit plan.

Conclusion

Equity lines of credit secured by commercial property provide a powerful tool for small business owners seeking flexible financing to seize growth opportunities.

CEOCs offer distinct advantages over other financing options like term loans, credit cards, and SBA loans for certain situations. But smart utilization requires understanding eligibility requirements, prudent use cases, tax optimization strategies, risk management planning, and negotiating favorable terms with reputable commercial equity lenders.

With the proper diligence and oversight, tapping into your commercial equity provides fuel to accelerate your business growth and profitability.

Quiz: Equity Line of Credit on Commercial Property

Gerry's commitment to helping businesses thrive is evident in his track record of providing tailored financial guidance. He understands the unique challenges that companies face and is dedicated to finding innovative solutions to support their growth.

When he's not working with clients or exploring the dynamic world of business financing, Gerry enjoys staying updated with industry trends and sharing his insights through informative articles. His passion for empowering businesses with financial knowledge is a driving force behind his work.

Connect with Gerry Stewart to tap into a wealth of financial expertise and unlock opportunities for your business's success.